Decoding fintech: the story of a disruptive sector

-by Hoang Anh Phan

As a second-year student at Dalhousie University, I am an intern supporting marketing and communications at Venn Innovation, the not-for-profit supporting innovation-based economic development in New Brunswick. Venn powers Atlantic FinTech, and during my tenure here, I got to work very closely with Alicia Roisman Ismach, the Head of Atlantic FinTech, and other fintech innovators and entrepreneurs in the region.

I started here as someone who did not know about fintech. Through all the work I did here over the last three months, and the countless conversations with Alicia and our region's fintech entrepreneurs, I've come to appreciate how tech innovation can impact the financial industry and our economy. What surprises me every day is that few companies identify themselves as fintech, though we see others having a financial component or connection.

Apart from that, there are companies that have an opportunity to add fintech components to their business model but may be unaware of the benefits of doing so. I sat down with Alicia Roisman Ismach to uncover, both, my curiosity, and the potential of the region

Alicia Roisman Ismach

Head of Atlantic FinTech

You have always said our region has many fintech companies, and that it is not about creating an ecosystem from scratch but is about nurturing and growing it. What is your definition of fintech? What is the filter you use to check a business is fintech or not?

Alicia: In my definition, fintech is the presence of a financial component that is critical for the success of some tech-based companies. That financial component may be part of their clients’ system, not necessarily their own, or can be provided to them by a partner. If a company gains benefits by adopting fintech strategies, then their growth path and company value are not only about their sales. It is about how the infrastructure allows them to grow faster, and be more profitable and increase their valuation.

My filter is the impact of that financial component on the solution or the sector. It could be the importance of the solution for the financial industry as a whole or could be the importance of the financial component for the solution. It is about how crucial that financial component or aspect is, for the company or their clients.

Do fintechs here not identify themselves as fintech?

Alicia: A tech innovation startup is built when an entrepreneur identifies a problem and starts building a solution for it. The solution can be composed of many different components. So, when the entrepreneurs describe themselves, they don’t do it according to industry definitions. They describe what they are doing, and that is how they identify themselves. Some will identify themselves as a software company. Someone else can describe the same business as a SaaS company, based on the distribution model of their solution. Others will describe themselves according to the industry they serve and the type of clients they have, or the clients they serve and markets or industry they are in.

The reason most companies in Atlantic Canada do not identify themselves as a fintech company is that this was not a popular term until very recently. It was, and is still, common to be described as ICT, software or AI and blockchain but not the sector that they are a part of. Fintech is lesser-known and most companies do not realize they have a financial component or something related to the financial industry that may benefit them.

Can you give us some examples for how a company can be fintech while also being a part of other industries?

Alicia: For example, consider an events ticketing startup. People will first describe it as a software company or a stakeholder for the events industry, but their solution has fintech components. They can take advantage of the model behind the fintech industry. Another example could be a company serving large manufacturers, many will describe them as enterprise solutions startup because of their clients although they can still be a fintech according to their model.

Another example would be a cybersecurity company, that can also be fintech depending on the clients they serve. This is the change in perspective that we want to bring.

Would this bring new opportunities for growth, for these companies?

Alicia: By identifying as fintech and start applying the relevant fintech strategies, they will be able monetize their services and improve profitability, increase their clients’ loyalty, and attract investments that are more in line with fintech valuations, that in average are higher than regular SaaS solutions. The reason fintechs can increase their clients’ loyalty is that they have the ability to be embedded more deeply into their processes, offering the client more benefits with the same solution, and making it harder to replace. A company that has this ability but does not recognize they are a fintech and strategize their growth path could miss the opportunity to apply strategies that could impact their future growth.

There may also be companies who have not used a financial component in their solution model so far but may be willing to explore in the future. If is relevant to their solution and markets, they would enjoy the same benefits I just mentioned.

What has led to the development of the fintech ecosystem in Atlantic Canada?

Alicia: It all started with the call centres and backend operations centres for large organizations like banks, communications companies and insurance, healthcare companies, among others. These centres have strong payment and billing components, and that is the very basics of fintech. Over time, fintech knowledge started flowing in the region and now there is unbeatable understanding about the problems, gaps and needs, what’s not working efficiently.

Our entrepreneurs and innovators noticed these problems and started developing solutions because they understood both the technology and the problem very well. This started a trend, and our region became home to many startups dedicated to backend systems, while many regions in the world focus on the front side because their understanding of consumer experience is better, for the most part.

So, solutions we build here can be used anywhere in the world. Is that correct? What are the opportunities outside the region for our fintechs?

Alicia: If the solution is tech-based, it is possible for a company to be based anywhere and to grow globally from there. For instance, Verafin has been working with global banks and they are a multibillion-dollar company recently acquired by Nasdaq. Another advantage to having a fintech company in Canada is the proximity to a market like the US. Entrepreneurs need to understand that their location does not determine their growth potential and opportunities.

Mission to Money20/20 in Las Vegas, 2019: Alicia with fintech founders and entrepreneurs from Atlantic Canada

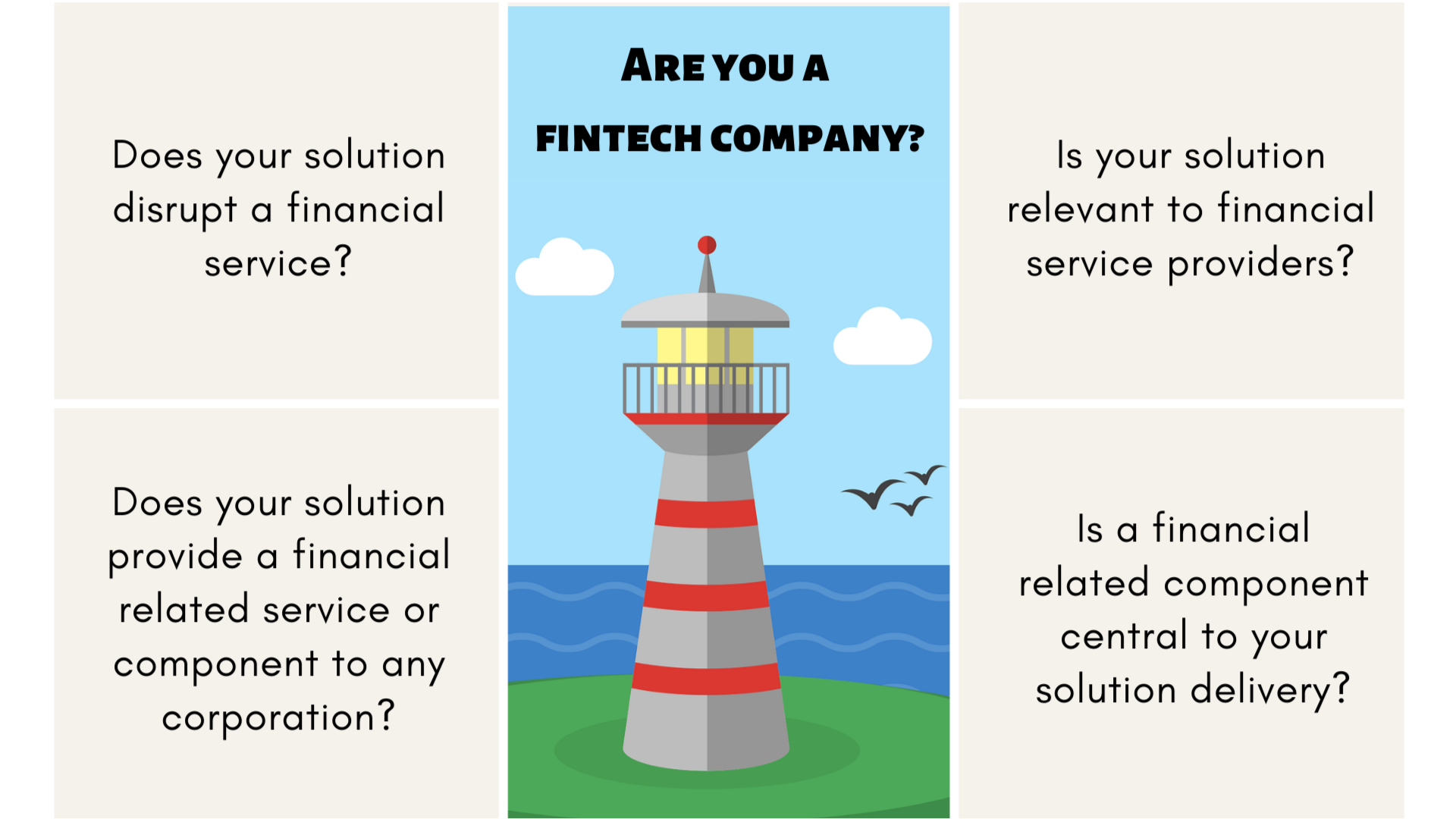

What’s the best way to know if you are a fintech company or not?

Alicia: On our Atlantic Fintech website, there is a simple 4-question quiz that companies can take to see if they are fintech. It will take less than a minute and is straightforward.

{kind=link}

If someone is unsure if they are fintech, even after they go through the checklist, what can they do to confirm?

Alicia: They can reach out to us and we’re happy to have a discussion.

This interview is by Hoang Anh Phan, summer 2021 intern in marketing and communications at Venn Innovation. Hoang Anh is doing her Bachelors in Commerce at Dalhousie University and is passionate about telling the stories of Atlantic Canada's tech-based entrepreneurs and innovators.